If you dream of mastering your finances and achieving financial freedom, learning how to optimize your personal finances is important in your personal growth journey.🚀

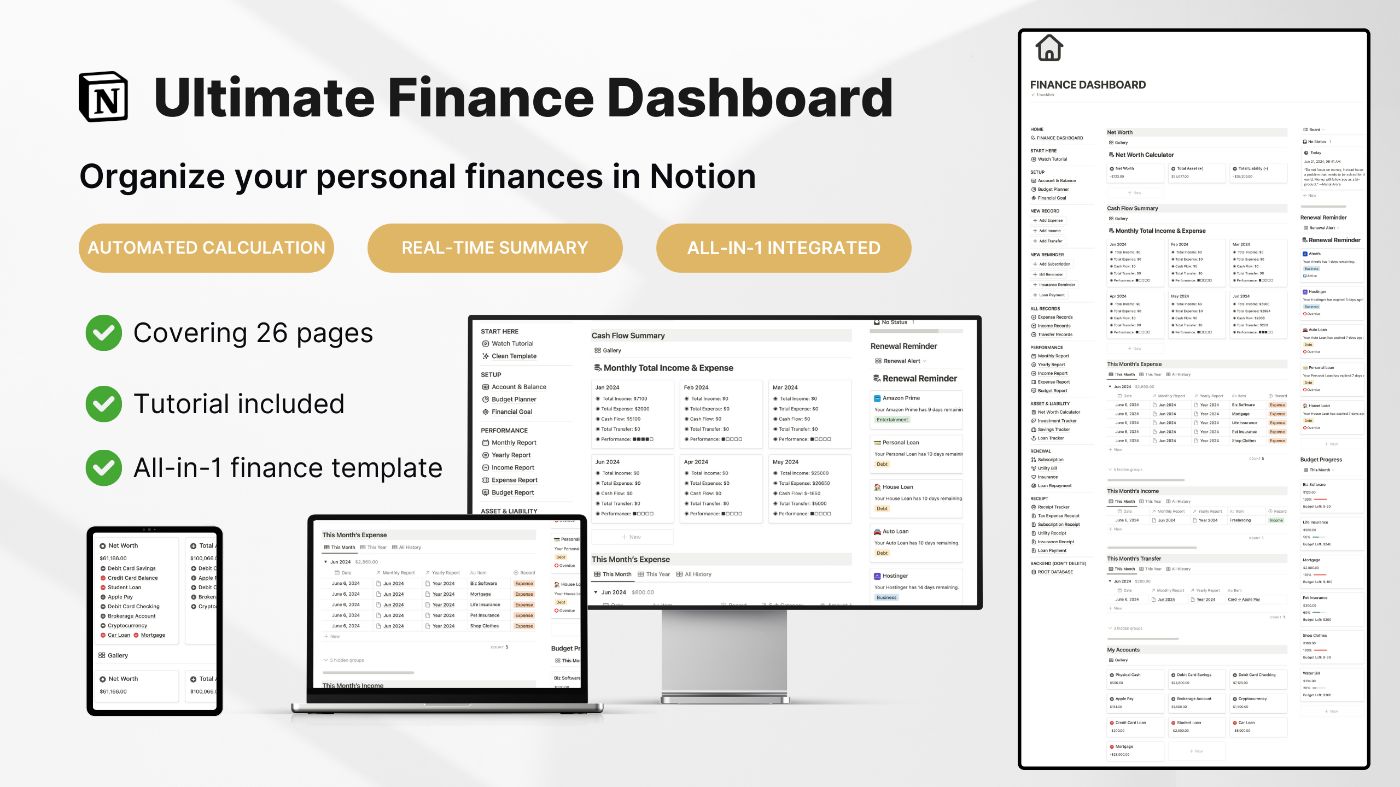

Today, I will share what I’ve learned over the past six years of my personal finance journey. I’ll also include my ⭐️Notion finance tracker (available on my personal website) that helped me achieve my financial goals faster.

If you prefer a video lesson, watch the video below: 🌟

https://youtu.be/GELIxZksPUM?si=FTKN9TGaAxiYc0yB&embedable=true

1. Create a Budget and Stick to It

Dang, where did those unexpected expenses come from?

Without budgeting, you’re flying blind with your finances. Because you’re always guessing where your money went.

One popular budgeting principle is the 50/30/20 rule.

This means you set aside:

- 50% of your monthly total income for needs (housing, groceries, utilities)

- 30% for wants (entertainment, shopping, lifestyles)

- and 20% for savings and investment

Of course, there are several variations to the 50/30/20 rule. Feel free to modify them based on your personal goals.

My Favorite Variation Is the 35/50/15 Rule:

- 35% is for Paying Yourself First, with 20% going to savings (emergency funds, general savings) and 15% to investments.

- 50% is for Essentials, with 30% for spending on needs and 20% for loan repayment.

- 15% is for Wants (dining out, vacation, entertainment, shopping)

I prefer the 35/50/15 ratio because it reduces spending on wants and increases savings and investments. This helps me build a stronger financial foundation compared to the 50/30/20 rule, which allocates a significant 30% to lifestyle expenses.

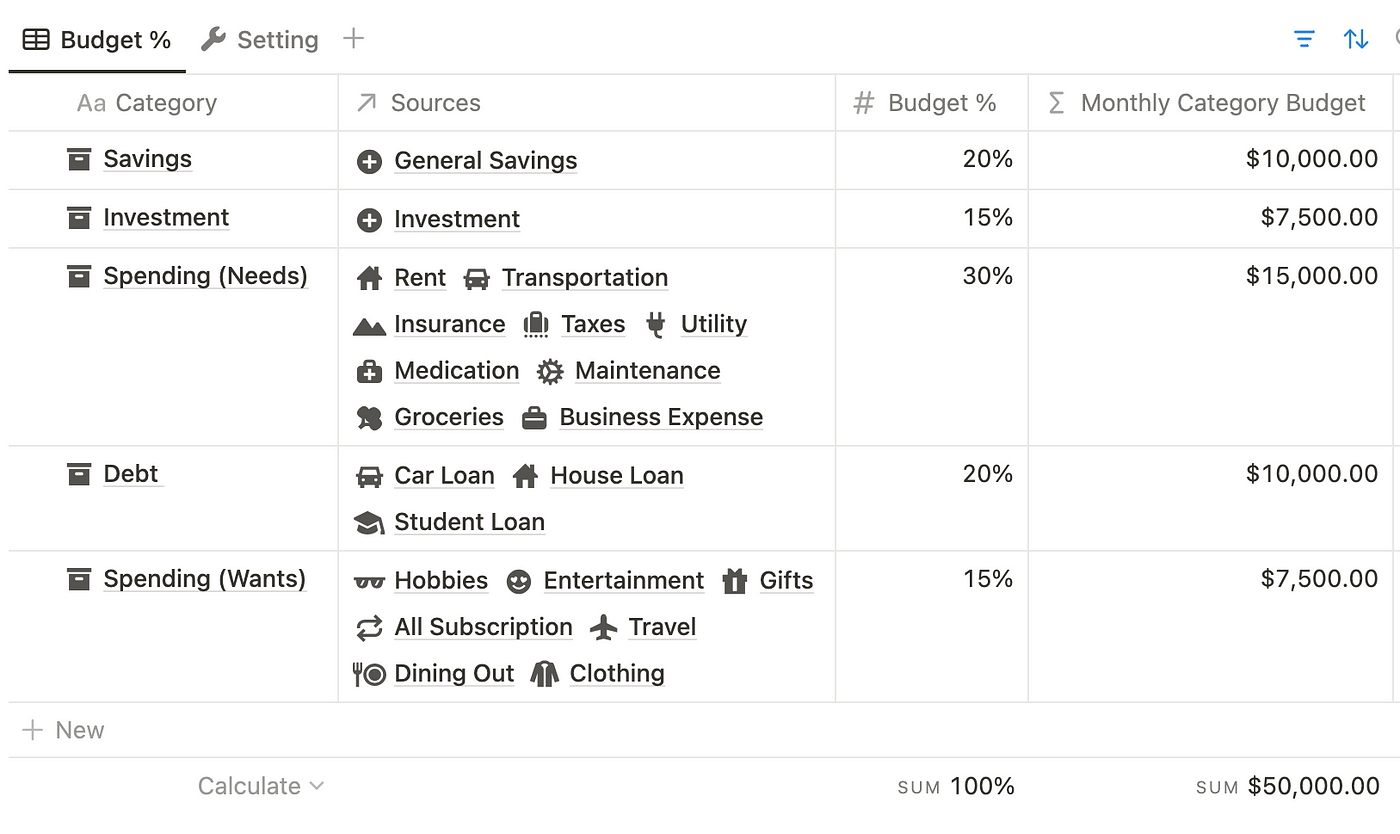

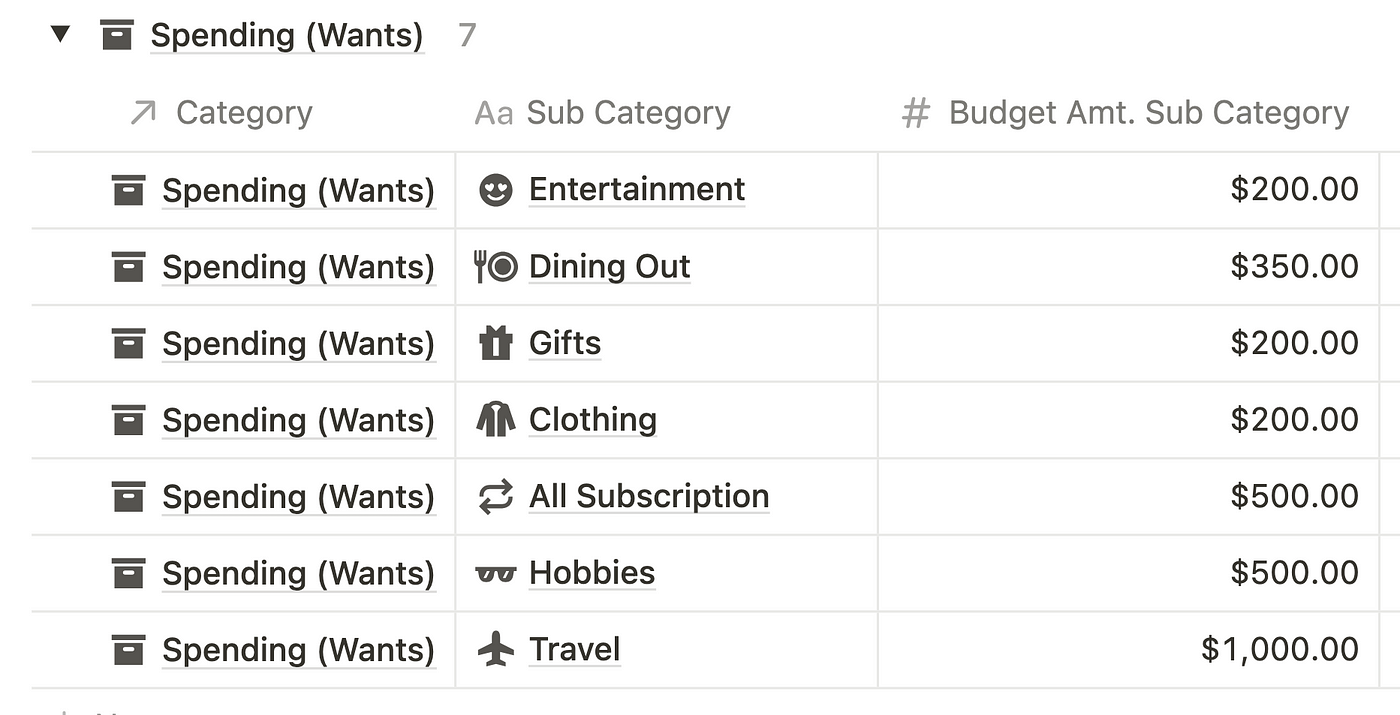

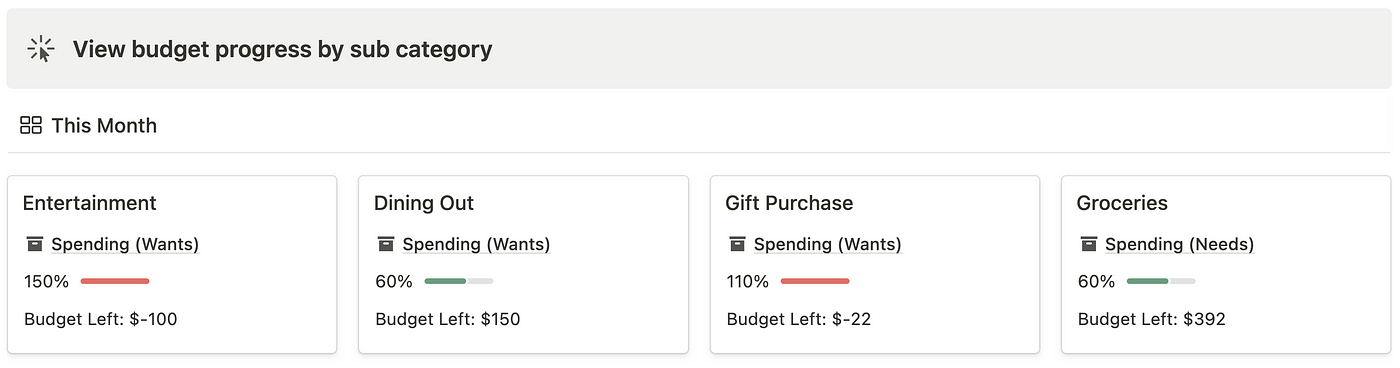

Plan Your Budget

Having a place to plan your budget is also important. I love to plan my budget using Notion. In my budget planner, I can use the budget calculator to allocate the % for categories like savings, investment, needs, and wants.

Then I can break it down further by specifying how much I want to spend every month on each subcategory. To do this, you can set up a budget planner like this:

2. Prioritize High-Interest Debt

Before taking on debt, it’s important to ask yourself these questions:

- Can you differentiate between good debt (which generates income over time) and bad debt (spent on consumer goods or depreciating assets)?

- Are you buying a home that you can easily afford, even if there are unexpected changes to your job or business?

- Are you applying for another auto loan while your existing car is still in good condition?

- How will this loan impact your long-term financial goals and stability?

Next, prioritize paying down high-interest debt so that you can save money in the long term by eliminating it more quickly.

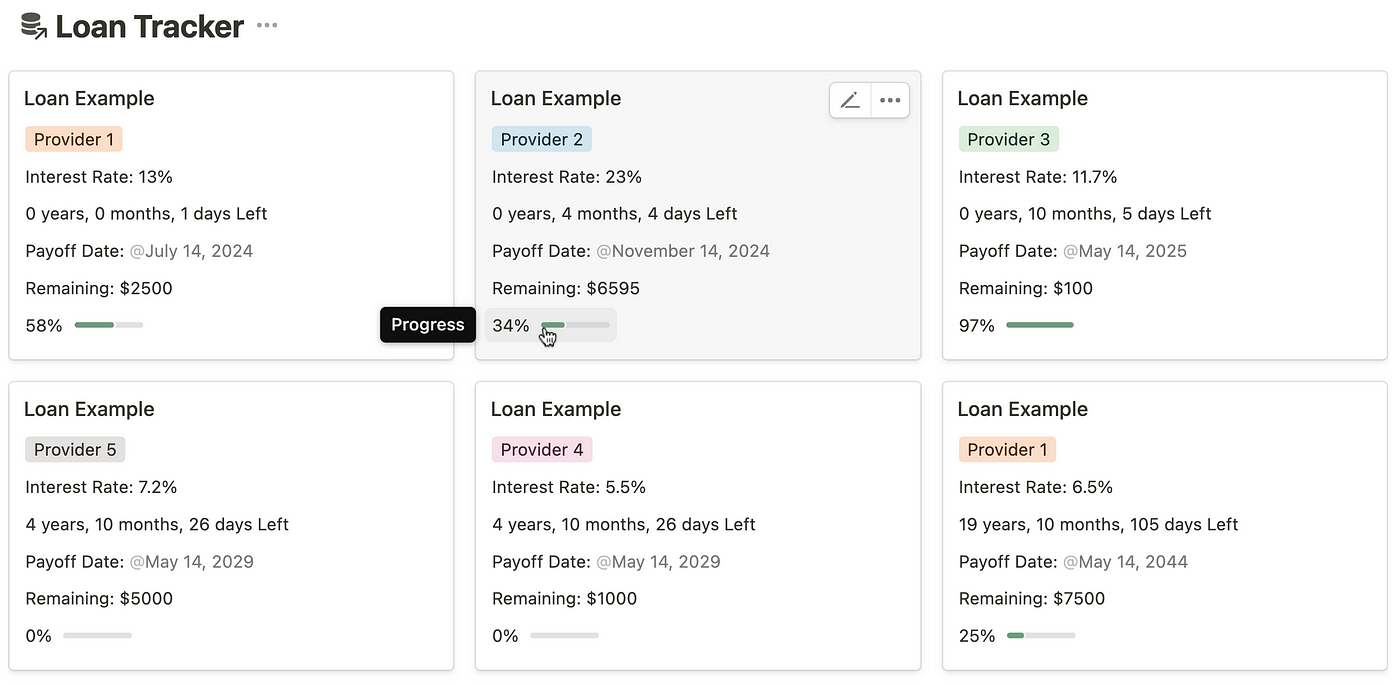

You can create a loan tracker and specify these details to keep track:

- Date started and completed, Provider, Loan amount, Interest rate, Duration of the loan, Monthly repayment amount, Remaining balance, and Percentage paid or progress

In my Notion loan tracker, I created custom formulas that automatically aggregate and calculate my monthly payments. It also includes a progress bar to motivate me as I work to reduce my debt:

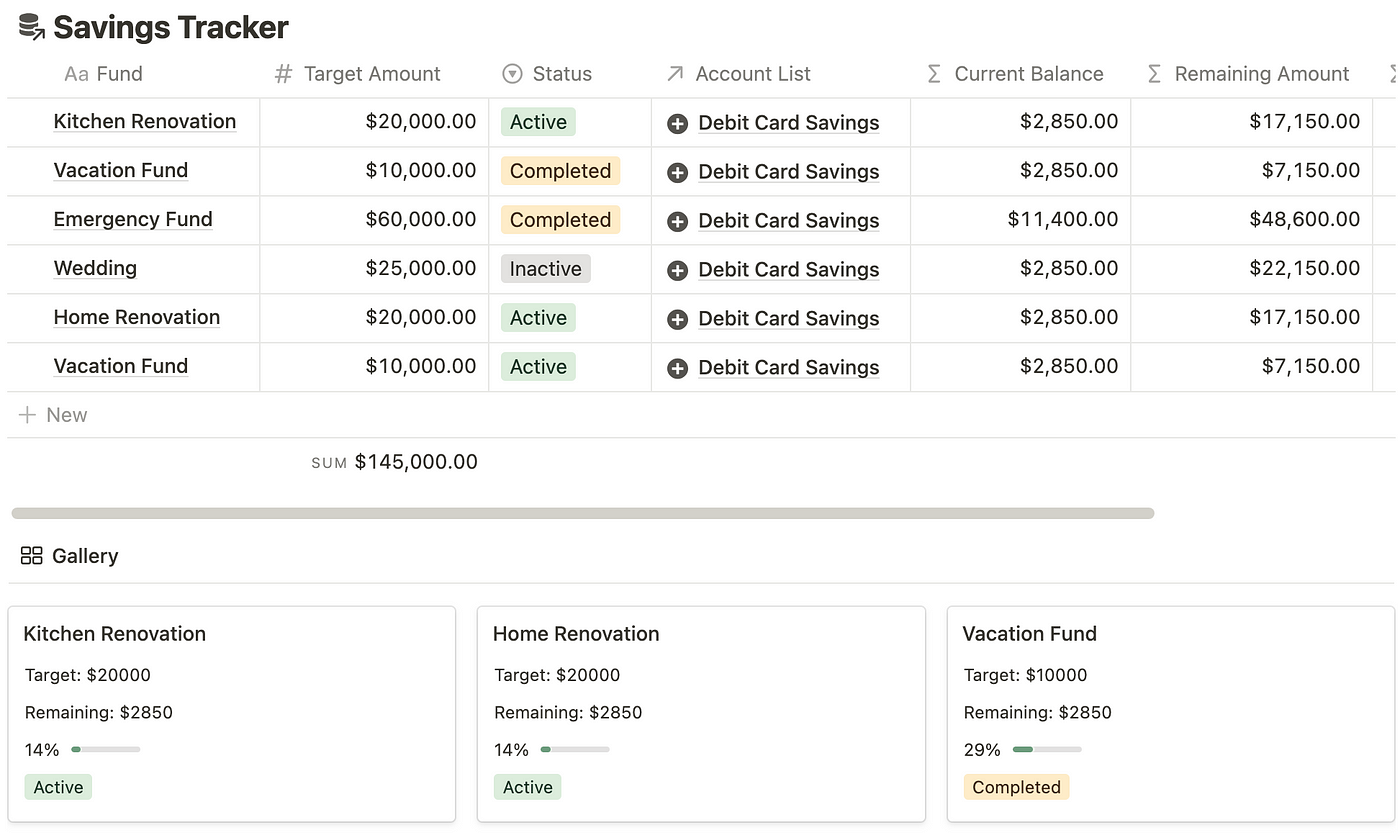

3. Create Sinking Funds

Creating sinking funds means setting aside money for future expenses or goals, allowing you to spread out the cost over time.

This approach not only motivates you to save money toward your goals but also reduces financial stress when it comes time to cover those expenses.

Examples of Sinking Funds:

- Emergency Fund: Savings for unexpected expenses like medical emergencies, car repairs, or sudden job loss.

- Vacation Fund: Money set aside for travel and vacation expenses, including flights, accommodations, and activities.

- Home Maintenance Fund: Savings for home repairs and maintenance, such as fixing a leaky roof, painting, or appliance replacement.

- Car Maintenance Fund: Funds for regular car maintenance, such as oil changes, tire replacements, and unexpected repairs.

- Holiday Fund: Money saved for holiday-related expenses, including gifts, decorations, and special meals.

- Wedding Fund: Savings for wedding-related costs, including venue, catering, attire, and decorations.

- Education Fund: Money set aside for educational expenses, such as tuition, books, and school supplies.

Here’s a Sinking Fund Tracker I Created in Notion. Some Cool Features Include:

- Set Goals: Determine the amount needed and the timeframe to save before the expense occurs.

- Track Transfers: Monitor the transfer of funds from Account A to Account B.

- Progress Monitoring: Track how much you have saved and how much more is needed to reach your goals.

- Status Updates: Update the sinking fund status (active, completed, or inactive).

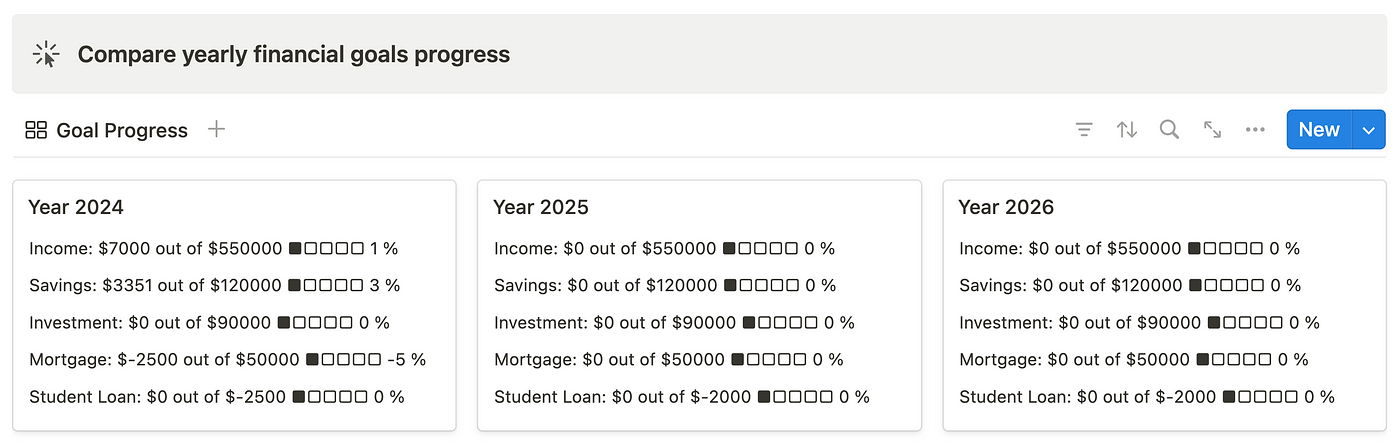

4. Set Your Financial Goals

Setting a specific target for money-related goals increases your chances of achieving them significantly.

Here’s How to Get Started:

-

Break down your money goals: Divide them into key areas such as income, savings, investments, budgeting, and debt repayment.

-

Create short-term and long-term goals: Establish immediate (within a quarter or year) and future goals. For example, aim to “save $25,000 for a down payment in 2 years.”

-

Be specific: Clearly define what you want to achieve, and ensure your goals are realistic and achievable within the specified timeframe.

-

Focus on one area each year: Concentrate your efforts on one financial area annually to maximize your energy and effectiveness.

Examples of Financial Goals Include:

- Income: Create 2 new income sources this year.

- Savings: Increase savings rate from 20% to 30%.

- Budgeting: Reduce non-essential spending by 15% this year.

- Investment: Achieve a 10% return on investment in the stock market by the end of the year.

- Debt Repayment: Decrease debt-to-income ratio from 35% to 20%. (e.g., By paying down $10,000 of auto loan while increasing your annual income by $5,000, you will reduce the debt-to-income ratio from 35% to 20%)

Personal Finance Challenges

In addition to numerical goals, consider setting qualitative goals or “Personal Finance Challenges,” such as:

- Achieving a ‘No-spend weekend’ once a month.

- Having ‘Low-buy months’ every other month.

- Achieving a ‘No-buy month’ three times a year.

- Implementing a ‘Free entertainment month’ by only engaging in cost-free leisure activities.

- Implementing a ‘Cash-only week’ every quarter.

5. Review Tour Finances Regularly

Regularly reviewing your finances helps you stay on track and make informed decisions.

Ideally, set a routine to review weekly, monthly, quarterly, and annually (EOY). Questions I always ask myself:

(1) Budget Limits and Progress:

Questions: Am I sticking to my budget limits for each category? Are there areas where I’ve overspent?

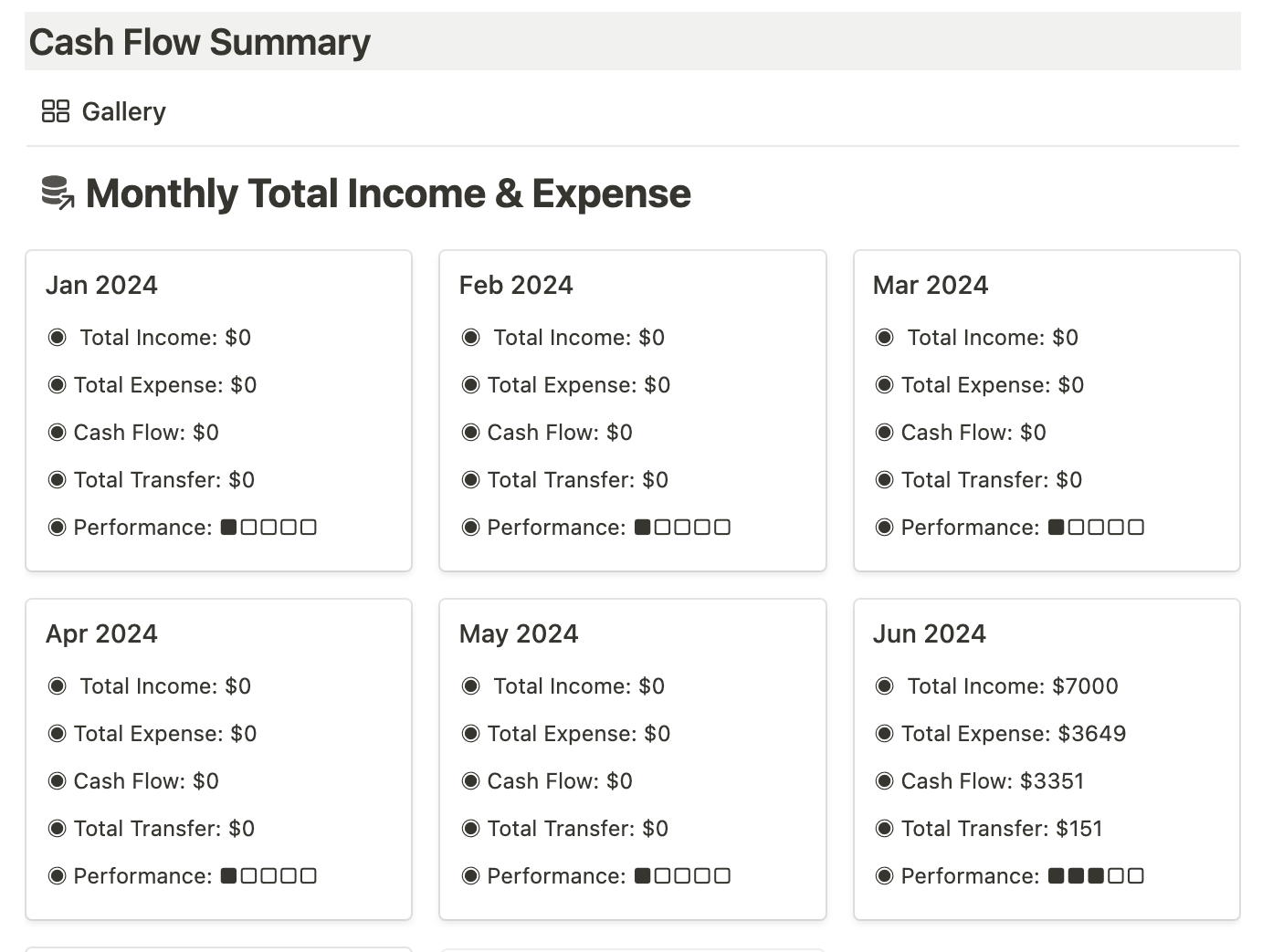

(2) Monthly Total Income and Expenses:

Questions: How does my actual income compare to my budgeted income this month? Did any unexpected expenses occur?

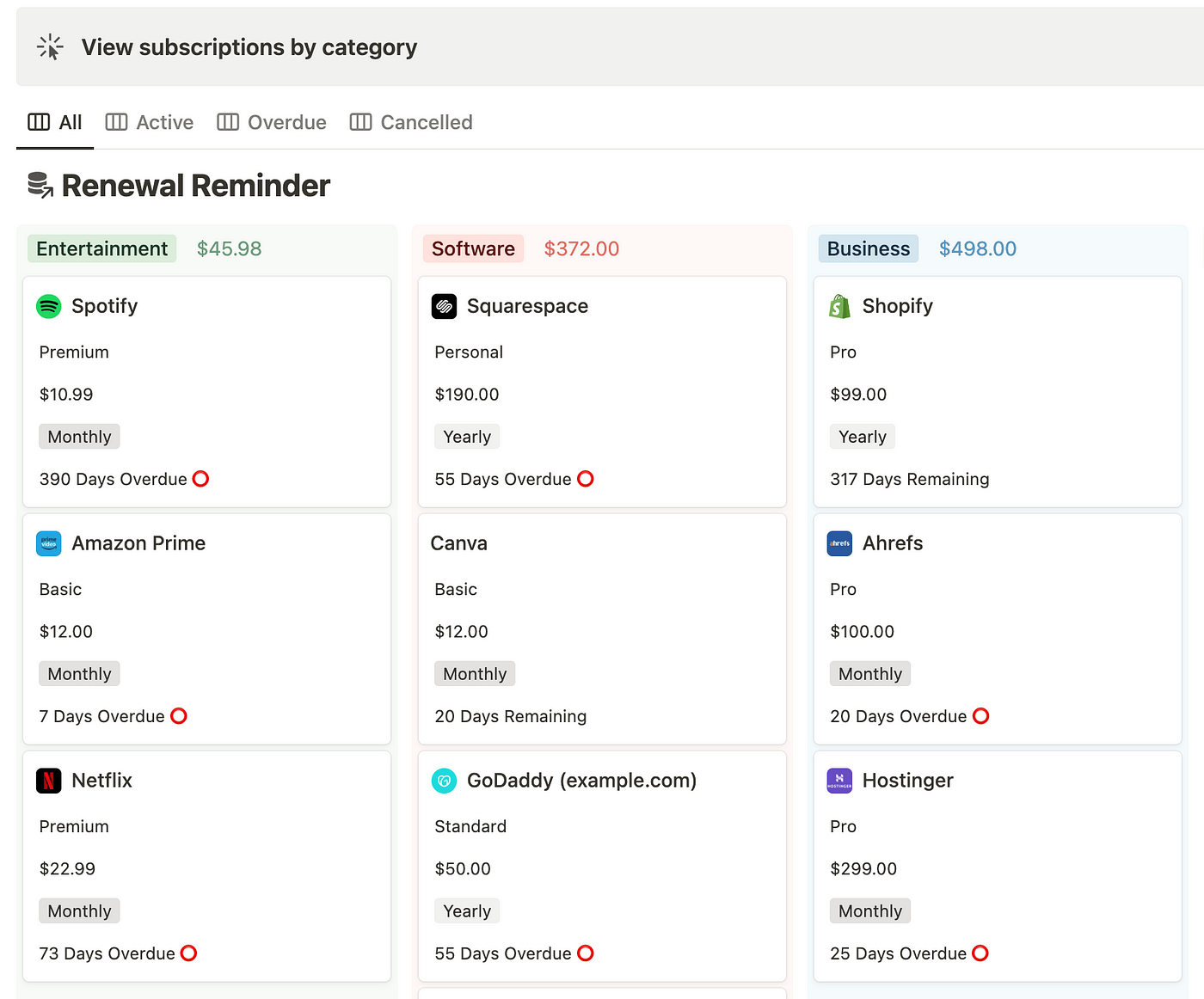

(3) Upcoming Subscriptions:

Questions: How many days are remaining before renewing X service? Are there any subscriptions due for renewal soon? Is there any subscription I want to cancel?

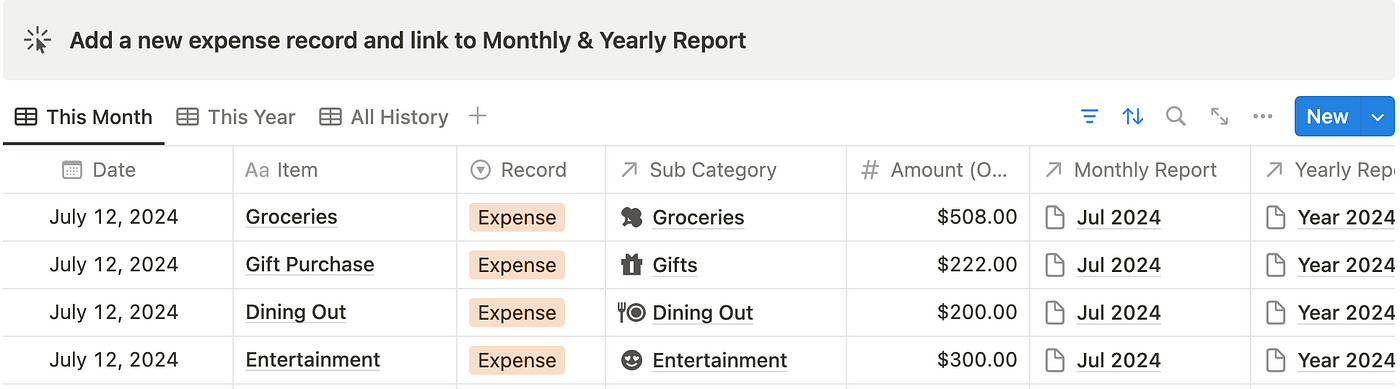

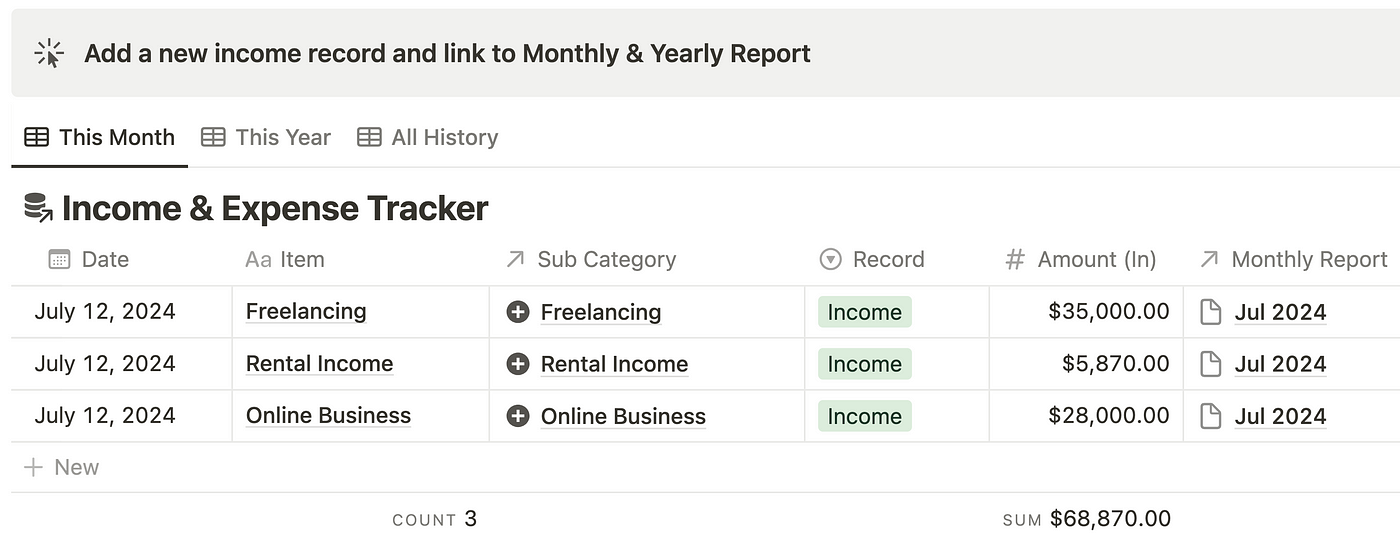

(4) Expense and Income by Categories:

Questions: Which expense categories have I spent the most on this month? How can I reduce expenses in any specific categories? How can I increase my income?

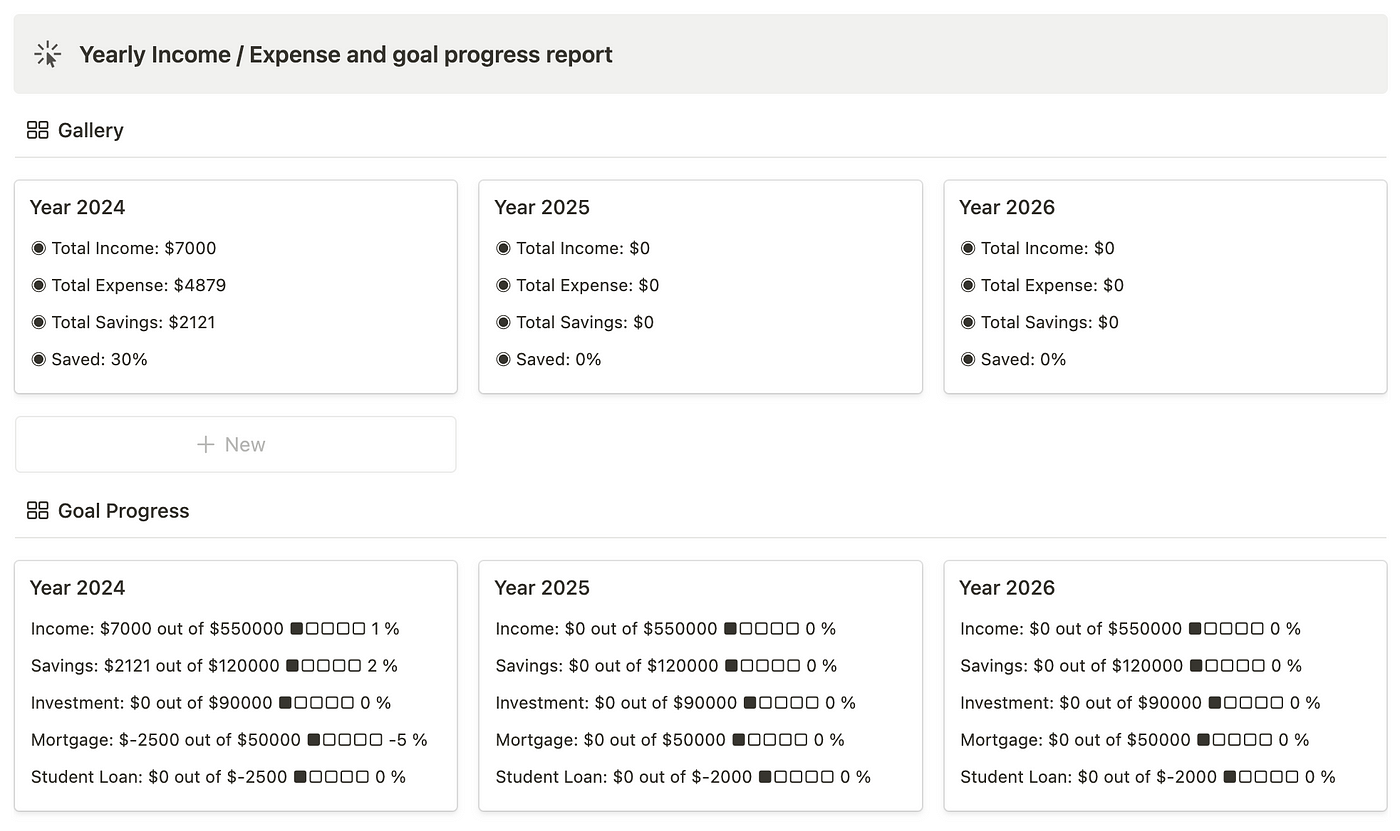

(5) Yearly Financial Goals:

Questions: How much progress have I made towards my annual financial goals? Do I need to adjust my financial goals for the next quarter or year?

Preview Full Finance Tracker

You can find the template tour on my personal website: https://whizzoe.com/#tools